84

85

Annual Financial Statements

At inception of the hedging transaction, the Group validates the hedging relation-

ship between the underlying and the hedging instrument as far as its risk man-

agement strategy is concerned. The Group also verifies the hedging efficiency

from the beginning of the hedging relationship and on a continuing basis.

All derivative financial instruments are initially recognized at fair value as at the

date of settlement and are valued on a mark - to - market basis on each balance

sheet date. The result of this valuation is recognized as an asset when positive

and as a liability when negative.

When a derivative financial instrument is no longer regarded as hedging instru-

ment any difference in its fair value is recognized in profit and loss.

There are three kinds of hedges:

A. Fair Value Hedging

Fair value hedging is regarded when hedging the exposure in the fluctuations of

the fair value of a recognized asset, liability, contingent liability or part of them that

could have a negative impact on results.

When hedging accounting, concerning fair value hedge, is followed then any

profit or loss from revaluation is recognized in profit and loss.

B. Cash Flow Hedging

The Group enters into Cash Flow Hedging transactions in order to cover the risks

that cause fluctuations in its cash flows and arise either from an asset or a liability

or a forecasted transaction.

On revaluation of open positions, the effective part of the hedging instrument is

recognized directly in Equity as “Hedging Reserve” while the ineffective part is

recognized in Profit & Loss. The amounts recognized in Equity are transferred in

profit and loss at the same time as the underlying.

When a hedging instrument has expired, sold, settled or does not qualify for

hedging accounting all accumulated profit or loss recognized in Equity, stays in

Equity until the final settlement of the underlying. If the underlying is not expected

to be settled then any profit or loss recognized in Equity is transferred to profit

and loss account.

C. Hedging of a Net Investment

Hedging of a foreign investment is regarded for

accounting purposes in a way similar to cash flow

hedging.

The effective part of the hedging result is recognized

directly in Equity while any ineffective part is recog-

nized in profit and loss. Accumulated profit or loss

recognized in Equity is transferred in profit and loss

account at the time of disposal of the investment.

Determination of Fair Value

The fair value of financial instruments trading in an

active market is defined by the published prices as

of the date of the financial statements.

The fair value of financial instruments not traded in

active market is defined through the use of valua-

tion techniques and assumptions based on relevant

market information as of the date of the financial

statements.

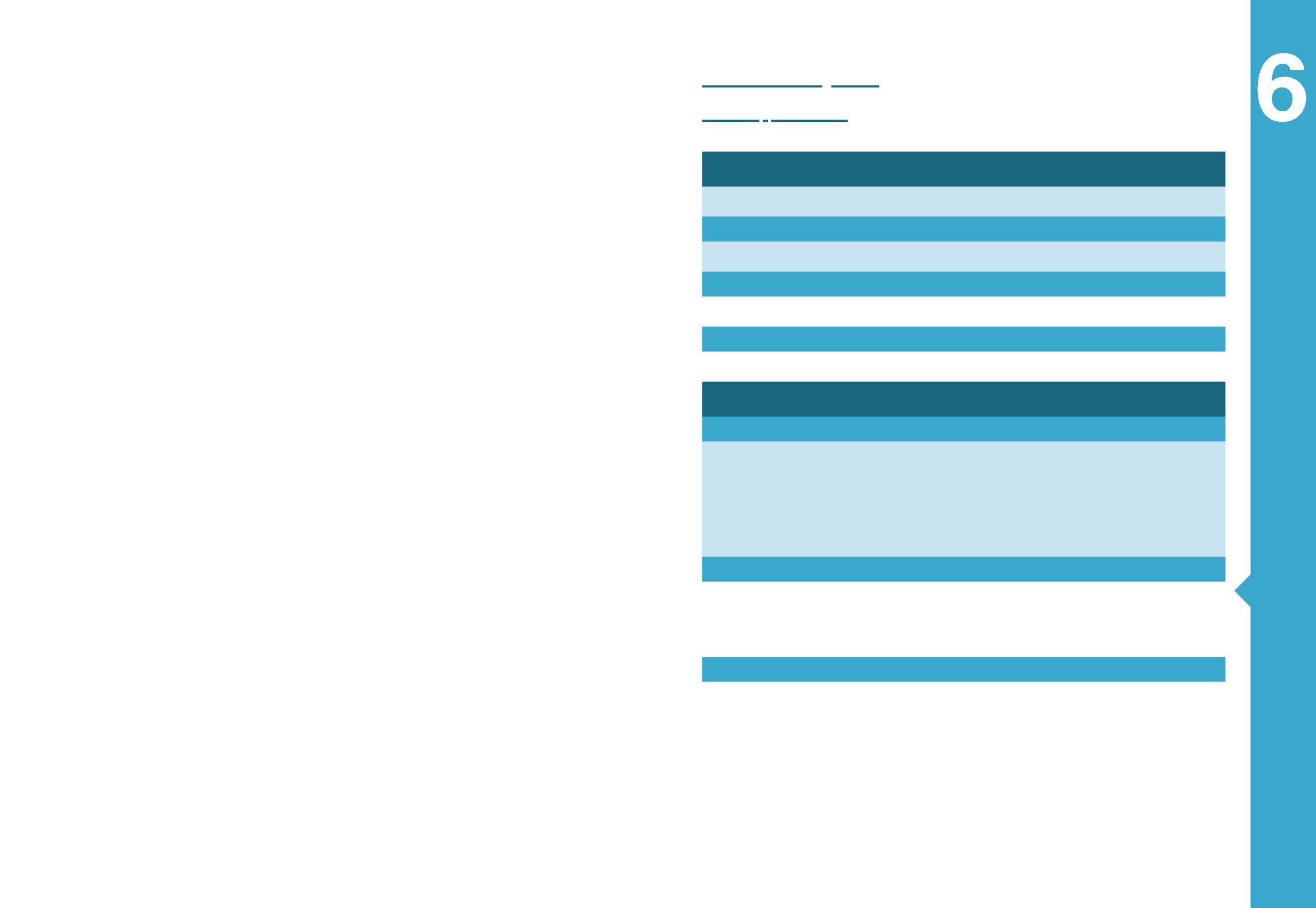

MYTILINEOS GROUP

(Amounts in thousands

€

)

Land &

Buildings

Vehicles &

mechanical

equipment

Furniture and

other

equipment

Tangible

assets under

construction

Total

Gross Book Value

391,140

1,386,321

31,656

22,078

1,831,195

Accumulated depreciation and/or impairment

(74,063)

(651,858)

(23,600)

-

(749,522)

Net Book Value as at

1/1/2014

317,077

734,462

8,056

22,078

1,081,673

Gross Book Value

389,660

1,384,596

32,822

41,630

1,848,709

Accumulated depreciation and/or impairment

(79,427)

(681,291)

(24,633)

-

(785,352)

Net Book Value as at

31/12/2014

310,233

703,305

8,189

41,630

1,063,357

Gross Book Value

398,105

1,417,786

33,839

56,646

1,906,376

Accumulated depreciation and/or impairment

(86,814)

(723,259)

(25,928)

-

(836,002)

Net Book Value as at

31/12/2015

311,291

694,527

7,911

56,646

1,070,375

(Amounts in thousands

€

)

Land &

Buildings

Vehicles &

mechanical

equipment

Furniture and

other

equipment

Tangible

assets under

construction

Total

Net Book Value as at

1/1/2014

317,077

734,462

8,056

22,078

1,081,673

Additions

3,937

11,972

1,076

32,463

49,448

Sales - Reductions

(154)

(1,398)

39

(8,019)

(9,533)

Depreciation

(7,413)

(43,899)

(1,477)

-

(52,789)

Reclassifications

425

4,369

830

(5,851)

(228)

Net Foreign Exchange Differences

2,510

16

6

527

3,059

Tangible Assets From Acquisition/(Sale) Of

Subsidiary

(6,149)

(2,215)

(341)

433

(8,272)

Merge Through Acquisition Of Subsidiary

-

(2)

-

-

(1)

Net Book Value as at

31/12/2014

310,233

703,305

8,189

41,630

1,063,357

Additions

3,779

35,843

812

35,264

75,698

Sales - Reductions

(22)

(14,574)

(9)

(384)

(14,989)

Depreciation

(7,411)

(47,219)

(1,402)

-

(56,033)

Reclassifications

2,357

17,160

329

(20,400)

(554)

Net Foreign Exchange Differences

2,356

13

(9)

536

2,896

Net Book Value as at

31/12/2015

311,291

694,527

7,911

56,646

1,070,375

4. Notes on the financial Statements

4.1 Tangible assets